How Does America Escape Its Fiscal Trap?

This article is part of The Boyd Institute’s quarterly policy sprint on the debt and deficit. To learn more about them and the work they do click here.

“History doesn’t repeat itself. But it often rhymes.” – Mark Twain

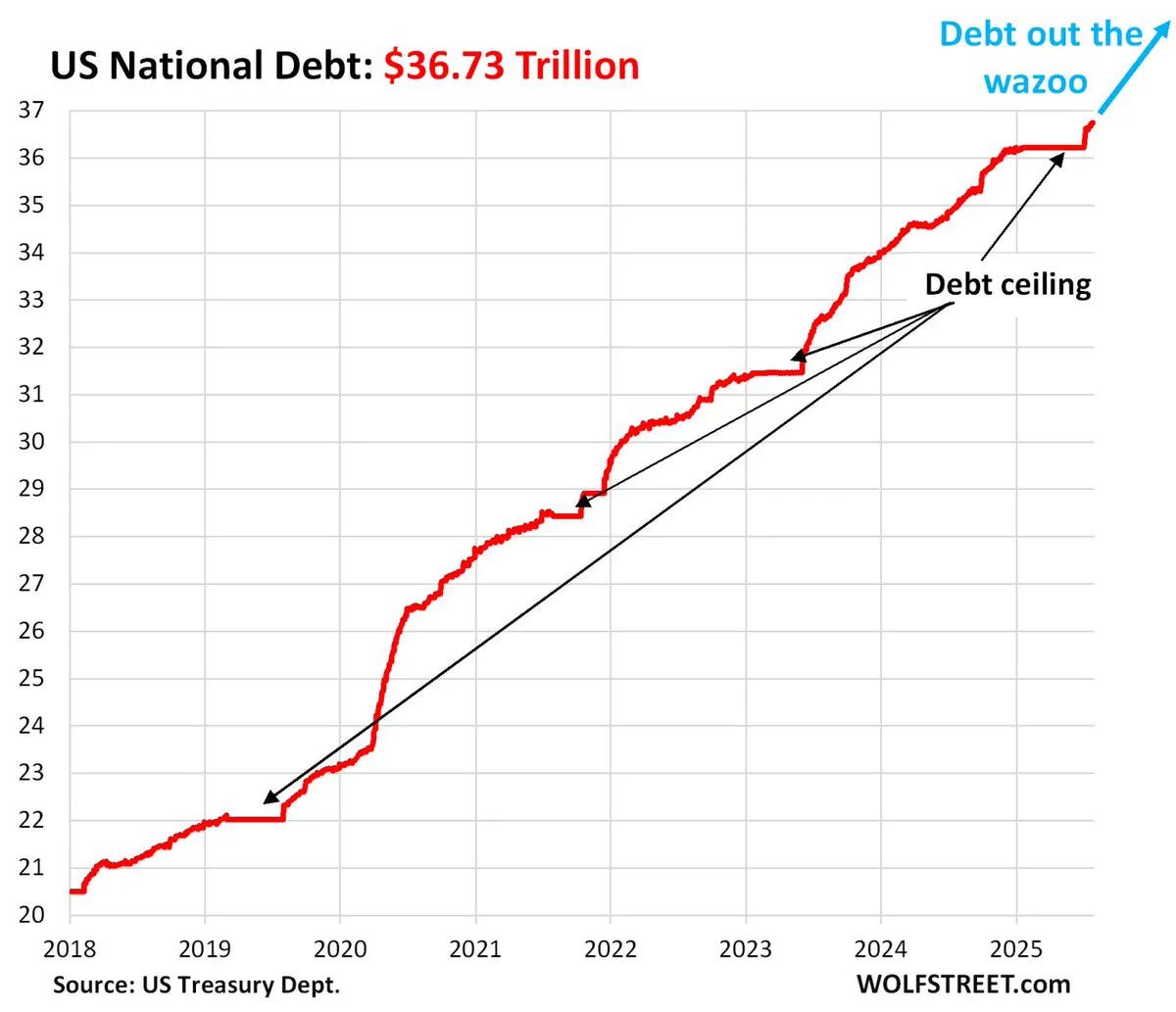

The United States national debt increases $70,000 per second. In the time it took you to read that sentence the National debt increased by $350,000. Houston, we have a problem.

In this essay, I’m going to explore:

Whether America’s debt “problem” is actually a problem. (Spoiler alert: It is.)

What we should do about it.

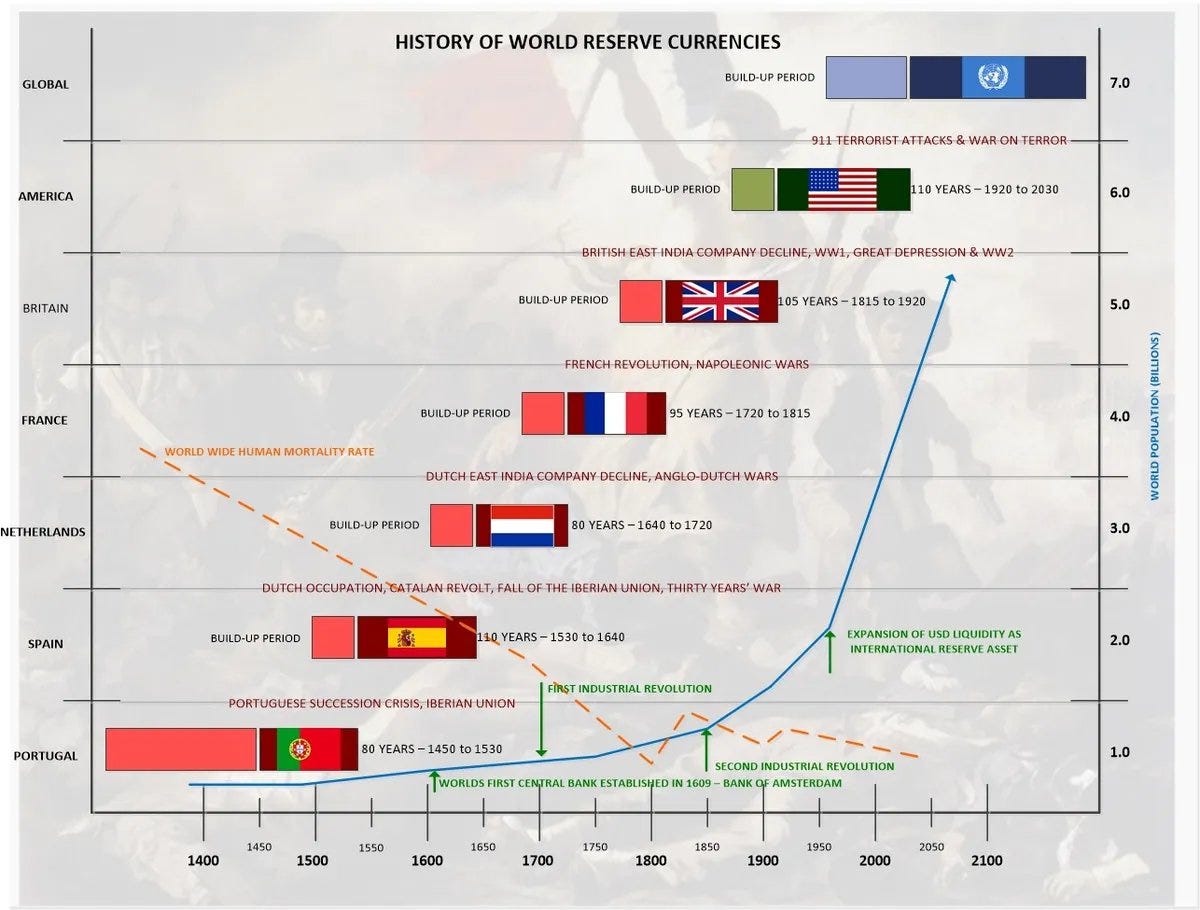

I. A Brief History Of Global Reserve Currencies

To figure out whether the U.S. debt “problem” is actually a problem, it’s useful to look at a brief history of national debt for countries who had the global reserve currency at the time.

National debt is a necessary evil for maintaining global reserve currency status.

1933: FDR passes the New Deal.

Following a landslide election, Franklin D. Roosevelt passed the New Deal during his First Hundred Days. In an effort to revive the economy post-Great Depression, he implemented social security for the first time.

1945: America wins World War II.

When WWII ended, the United States effectively won the global economy. At the 1944 Bretton Woods Conference, the dollar was pegged to gold – and every other currency was in turn pegged to the dollar.

1965: LBJ passes Medicare and Medicaid.

After winning the 1964 election, Lyndon B. Johnson passed Medicare and Medicaid.

1971: Nixon takes USD off the gold standard.

Richard Nixon takes the U.S. off the gold standard in 1971. The dollar (still the global reserve currency) became a fiat currency. Which means that it’s fully backed by full trust in our country — and more accurately, the strength of our military.

1978: The 401(k) is invented.

Ted Benna, a benefits consultant, realized a newly passed tax law allowed employees to contribute to retirement accounts with tax advantaged salary deductions. While it wasn’t the original intention, the IRC technically allowed for this.

1997: The Roth IRA is invented.

The Taxpayer Relief Act, sponsored by Delaware Senator William Roth, was designed to encourage retirement savings by allowing tax free growth of your investments.

2003: The HSA is invented.

The HSA, as we know it today, began in 2003 when George W. Bush signed it into law.

Historically, this broader context matters. Excessive spending on social benefits has already happened before. By looking at the past, we can infer how the future could look.

II. Wagner’s Law

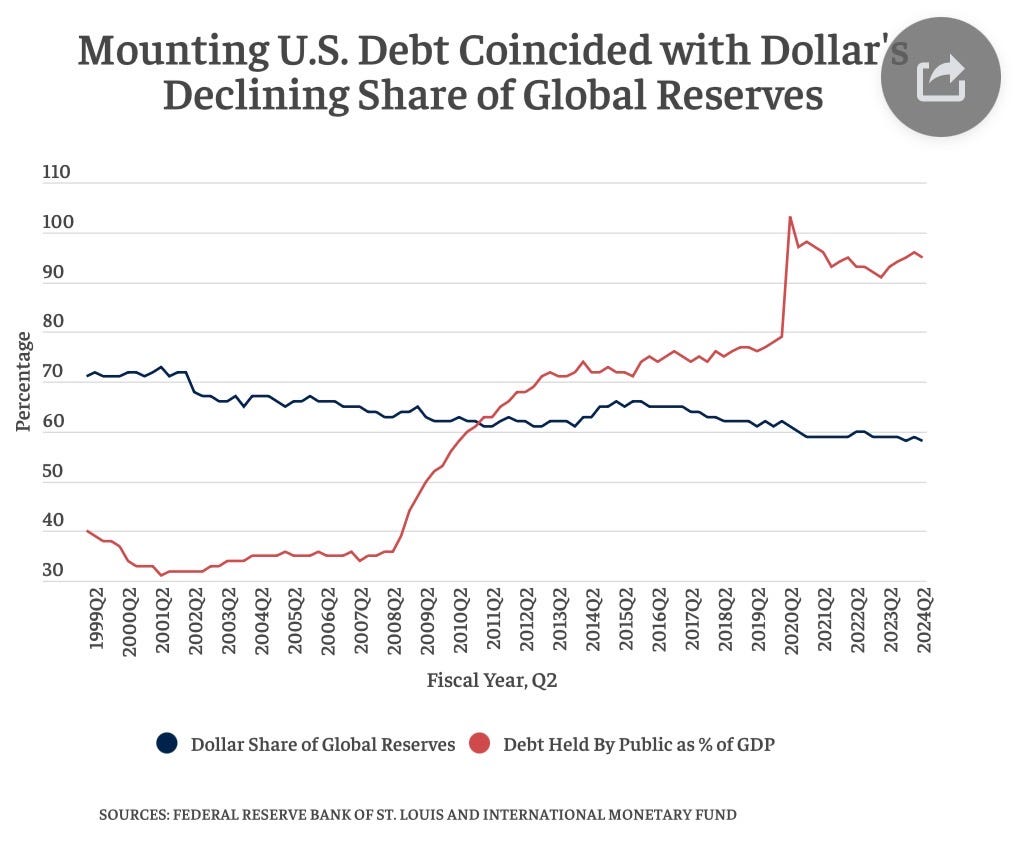

America’s growing debt is eroding trust in the U.S. dollar as a reserve currency.

In 1863, the German economist Adolph Wagner first observed something interesting in his homeland: public expenditure tends to increase as national income rises.

His observation suggests that welfare states evolve from free-market capitalism because the population votes for ever-increasing social services as income grows.

Starting in the 1920’s, and until after WWII, the British government dramatically boosted spending on social services. This led the UK to spend less on education, causing them to fall behind most Western Economies by the 1970’s.

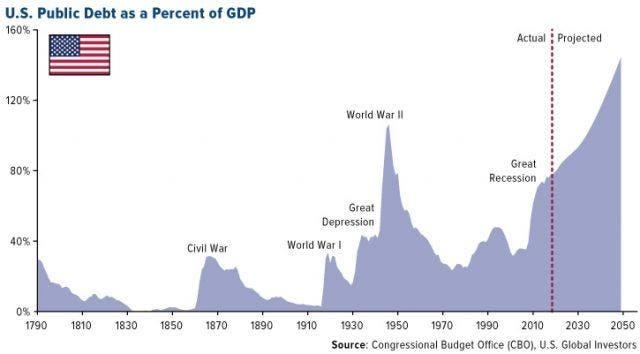

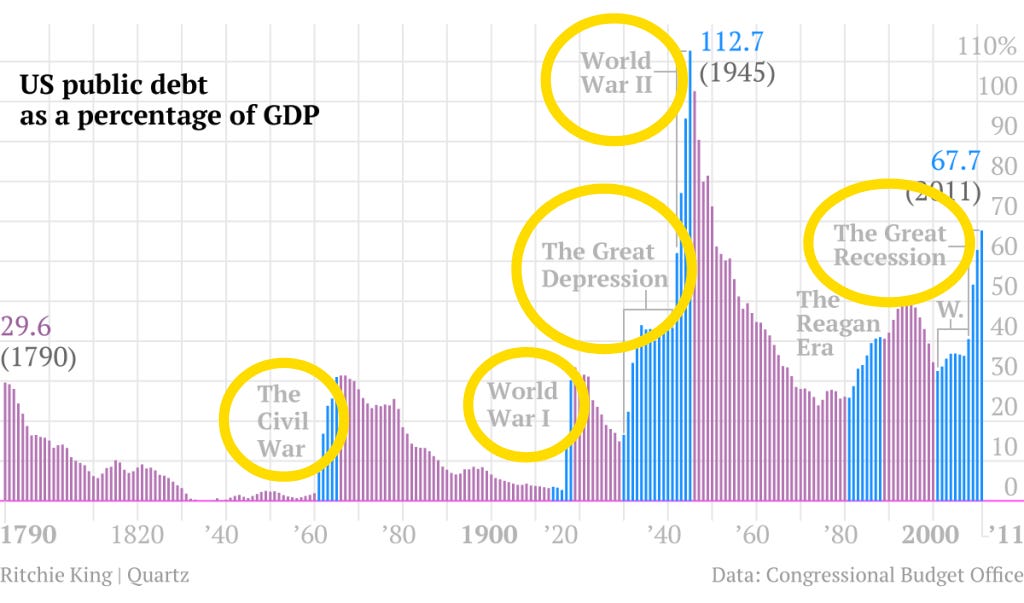

In 1961, Peacock and Wiseman made a key addition, by positing that public expenditure does not grow smoothly, but rather in spikes during social disturbances like wars and pandemics.

Since the 18th century, Wagner’s Law holds true in America:

Since 1980s, debt began to soar once again — but during peace time. The reason is three-fold:

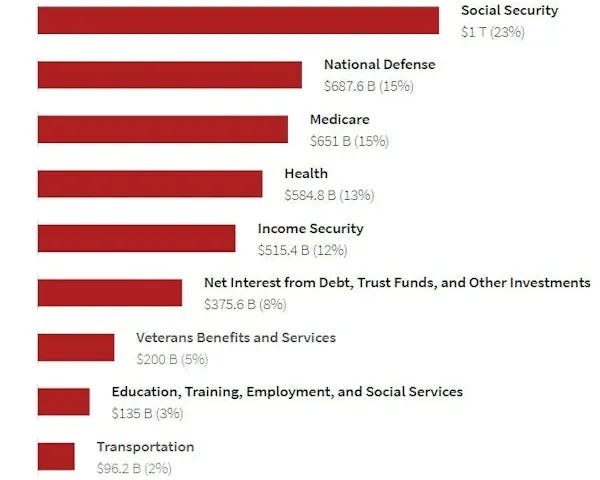

Aging population who the government spends on for social security and Medicare.

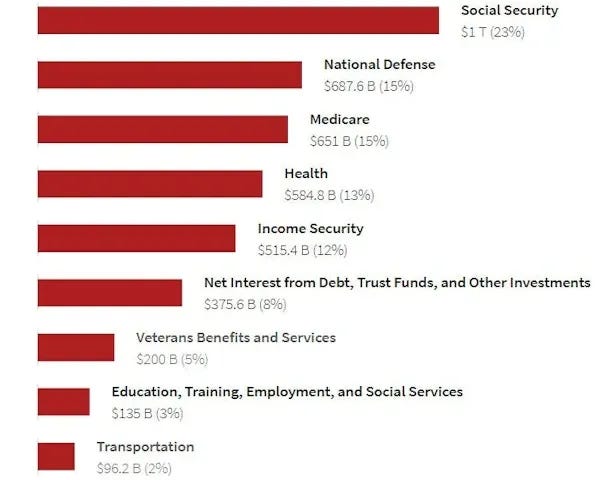

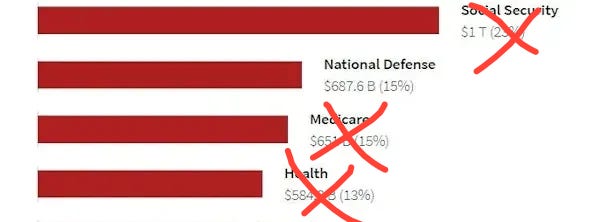

Current federal spending by category. Source Rising healthcare costs.

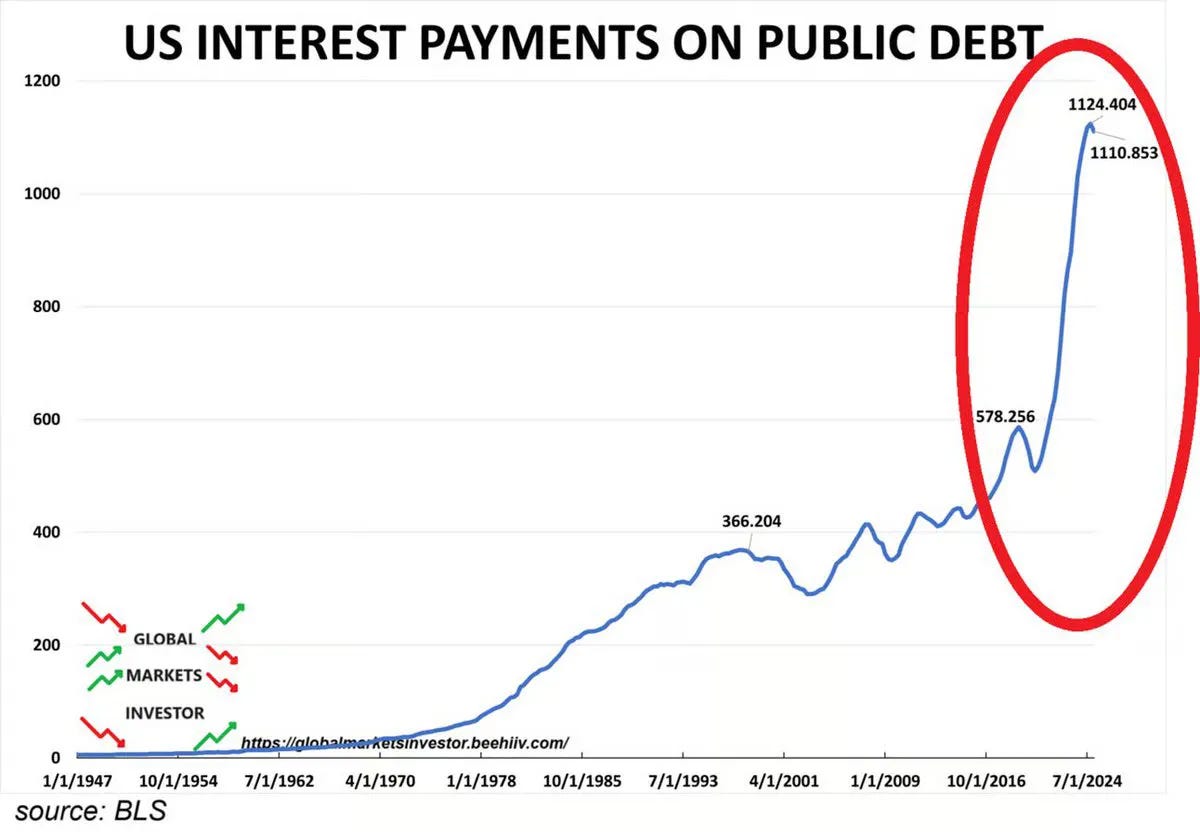

Escalating interest payments on the national debt.

How we’re racking up debt matters less than the fact that we are. The track we’re on is unsustainable if we hope to maintain financial dominance as we’ve had since post-WWII.

“The dollar and the military are inseparably linked — military power underpins trust in the currency, while the dollar’s privileges make it easier to finance that power.” — Former IMF Chief Ken Rogoff in Our Dollar, Your Problem

III. Why Debt Is A Big Problem For America

The biggest threat to the current world order is de-dollarization causing the USD to lose its status as the reserve currency.

The federal deficit is a serious problem.

Since Richard Nixon took the U.S. off the gold standard in 1971, the dollar became a fiat currency — backed by full trust in the U.S. military strength — which, by necessity, means we have to continue funding it.

Because the USD is the global reserve currency, we have the luxury of lower borrowing costs, which helps us fund the military.

Could lack of spending on military strength cause us to lose global reserve status? Or could spending on military and other things cause us to run up a deficit so high that value of the U.S. dollar lose the trust of other nations?

Unfortunately, it seems as though both could be happening right now.

In 2023, when the U.S. froze $300 billion of Russian assets during the Ukraine War, Middle Eastern energy producers began to hedge against total dollar dependence. Some nations like the UAE began accepting the Chinese Yuan for some transactions.

When I told my wife, who has family in Cairo, she matter of factly said, “They’re already talking about de-dollarization.” In 2024, Egypt announced it’d switch from USD to EGP as part of the BRICS de-dollarization program.

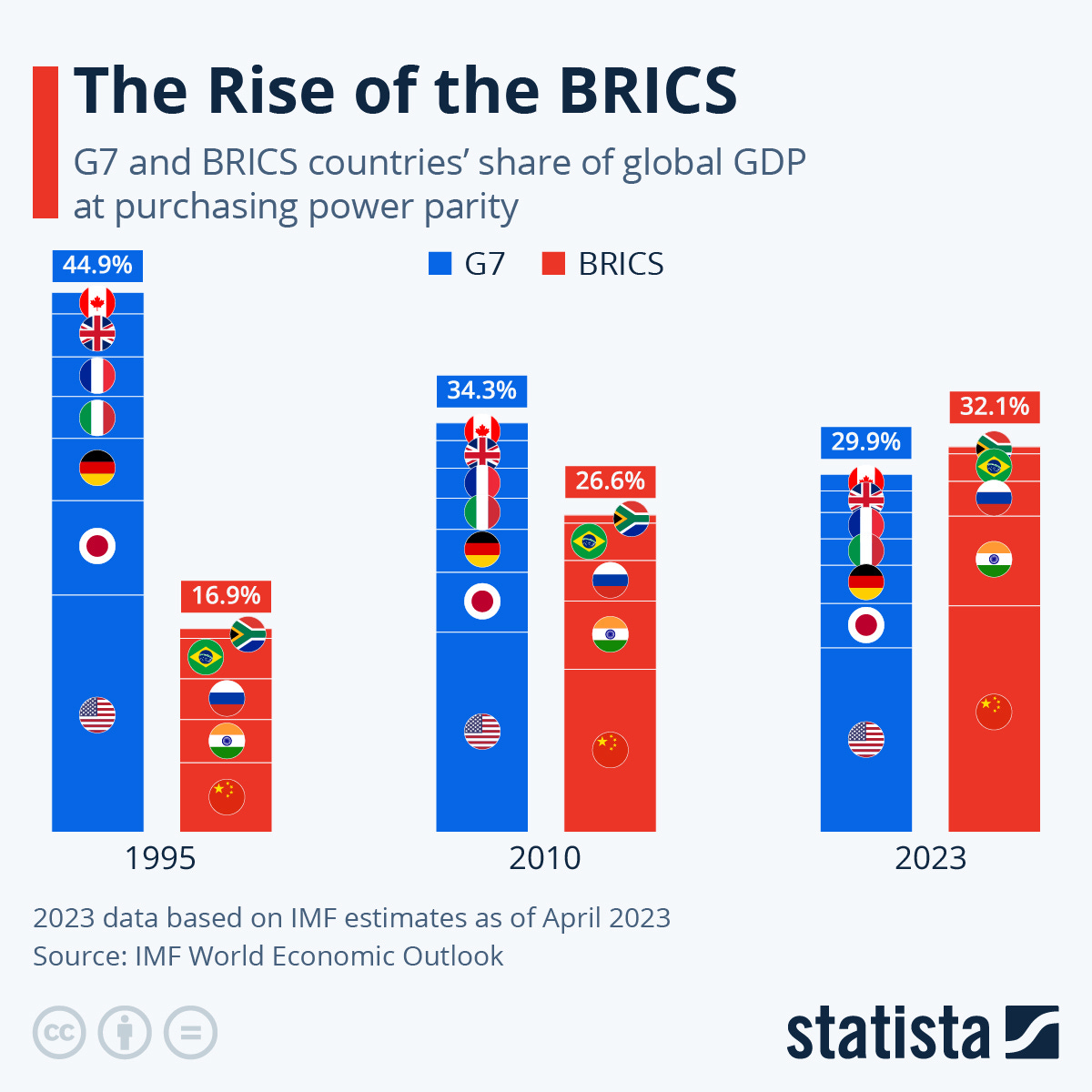

And by 2030, nations like Brazil, Russia, India, China, South Africa, and the UAE – collectively known as BRICS – will represent 50%+ of global GDP by 2030.

The Middle East is already de-dollarizing. If Iran successfully takes control of the Strait of Hormuz in 2026, that could be a huge blow to global confidence in the United States’ military, from whom the U.S. dollar’s value is derived.

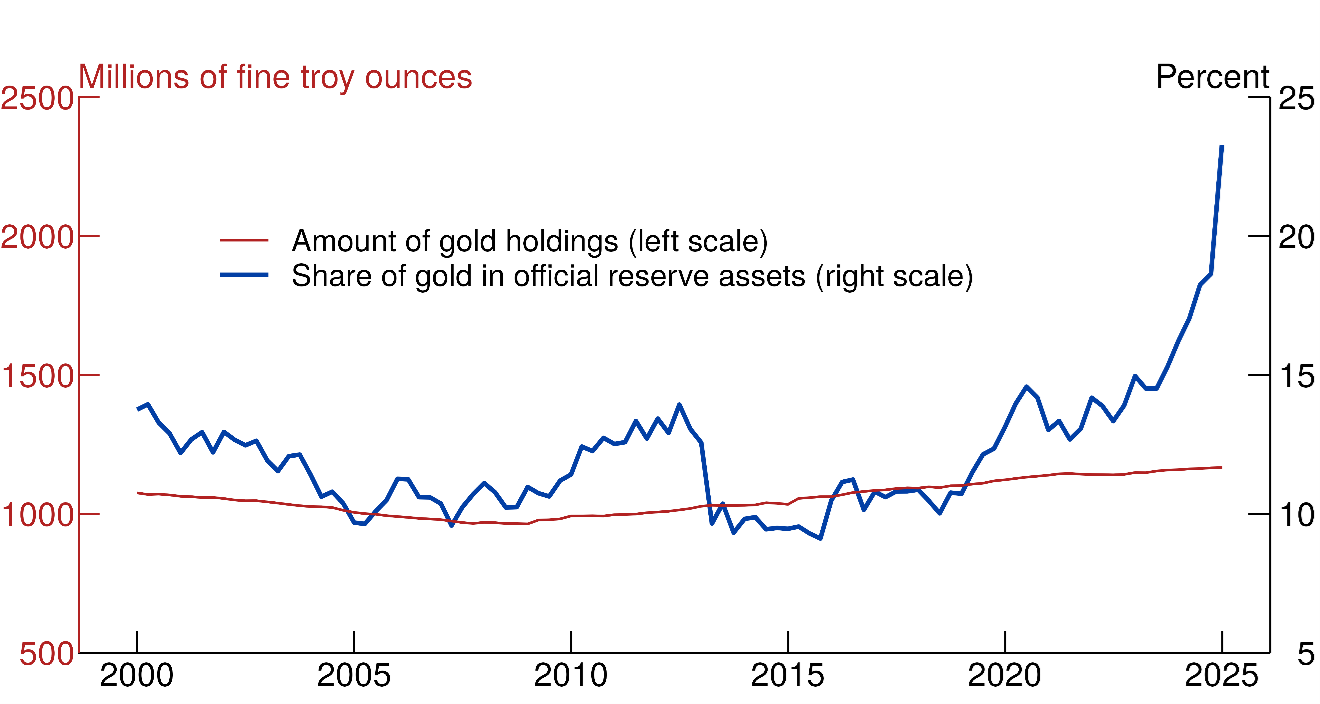

Domestically, the trend lines of confidence in the U.S. dollar isn’t much better. In May 2025 Moody’s downgraded the United States’ credit rating. The share of gold in official reserve assets has more than doubled from sub-10% in 2015 to over 23% now.

Which brings up an interesting ‘chicken or the egg’ dilemma. Could government spending on many things — especially our military — be eroding confidence in the dollar, thus shifting our status as the reserve currency? Or do we have to continually fund our military to maintain the strongest militia to preserve faith in the U.S. Dollar, without backing by the gold standard?

IV. What We Should Do About It

Roll back social benefits to reduce costs and let people fund their own retirement without government assistance.

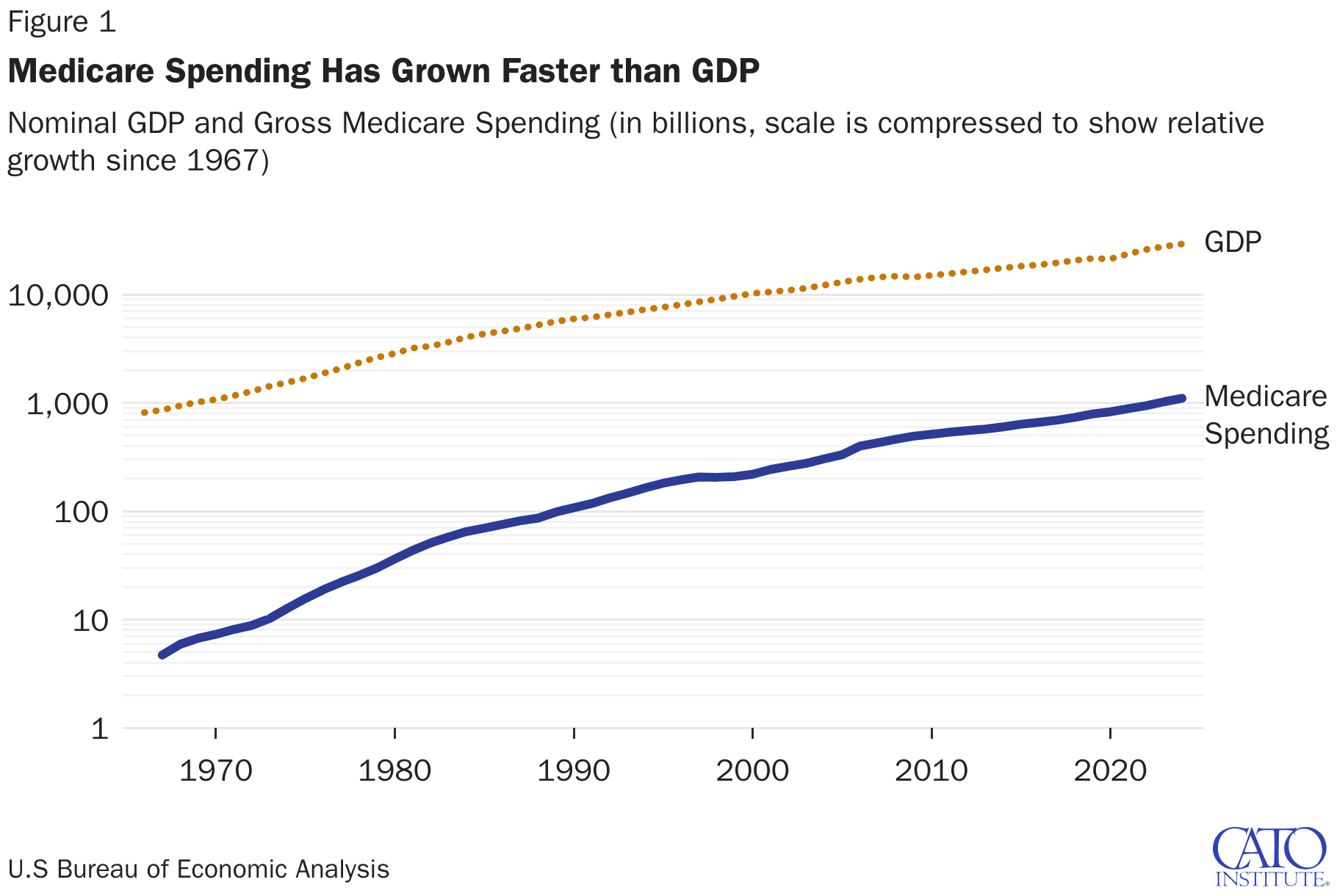

Anything the government subsidizes goes up in price. The federal government spends $2+ trillion on social security, Medicare, and health care annually. Because we ran a $1.8 trillion deficit in 2025, eliminating those expenses alone would put us in the green. And I believe it’d make healthcare more affordable because prices wouldn’t be propped up by federal government spending.

An interesting write up by the Cato Institute echoes this sentiment:

“Economic growth drives innovation and longer lifespans — but under Medicare’s open-ended design, those gains automatically translate into higher costs for taxpayers. As medical technology advances and Americans live longer, Medicare automatically pays for more treatments, more procedures, and more years of coverage, ensuring that program spending expands.”

— Cato Institute, Why We Can’t Outgrow The Medicare Driven Health Crisis

Mark Cuban also wrote an essay in which he describes all that’s wrong with healthcare today. His DTC pharmaceutical company, Cost Plus Drugs, is designed to transparently deliver maximum value to patients without the middle man taking a bite. America needs more upstarts like this making it affordable to get quality healthcare.

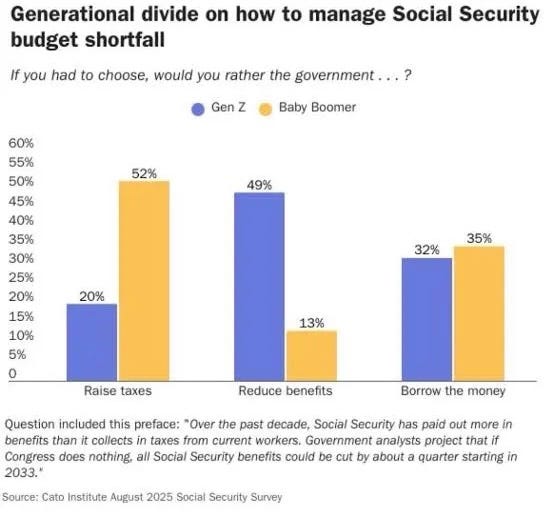

Teenagers — encouraged by their parents — are investing in stocks in droves. (WSJ) While not planned, the tax-advantaged retirement accounts — 401(k) (1978), Roth IRA (1997), and HSA (2003) are paving the way to eventually eliminate social benefits. I’m not alone in thinking this. Half of my fellow Gen Z brethren also think rolling back social security is the best way to handle the budget deficit.

Gone are the olden days where retirement income is provided by a company pension. Now we have 401(k), Roth IRA, and HSA’s. Gen Z is also investing sooner than boomers. Per Barron’s:

“Younger Americans are beginning to invest sooner than previous generations, thanks to increased access to investing and financial education, according to the latest Charles Schwab Modern Wealth Survey.

On average, Gen Z — generally described as those born between 1997 and 2012 — began saving and investing at 19 years old, according to the survey. Baby boomers — Americans born between 1946 and 1964 — didn’t start until age 35, on average.”

In other words, as a country, we’re not in a place to pull back on social benefits yet, but we’re on our way. But surely it can’t be that easy, right?

In A Theory of Justice (1971), John Rawls suggests that we imagine ourselves sitting behind a ‘veil of ignorance’ that keeps us from knowing who we are and our personal circumstances so that we can more objectively consider how society should be run.

The liberty principle requires that the social contract should ensure that everyone enjoys the maximum liberty possible without intruding on the freedom of others.

The difference principle asks that the social contract should ensure everyone has equal opportunity to prosper.

Under the ‘veil of ignorance’, the right time to eliminate social entitlements is never. If we’re redesigning a society without knowing our place in it — whether wealth, health, or socioeconomic status — we’d choose a framework that protects the worst-off, making the total eradication of safety nets unacceptable.

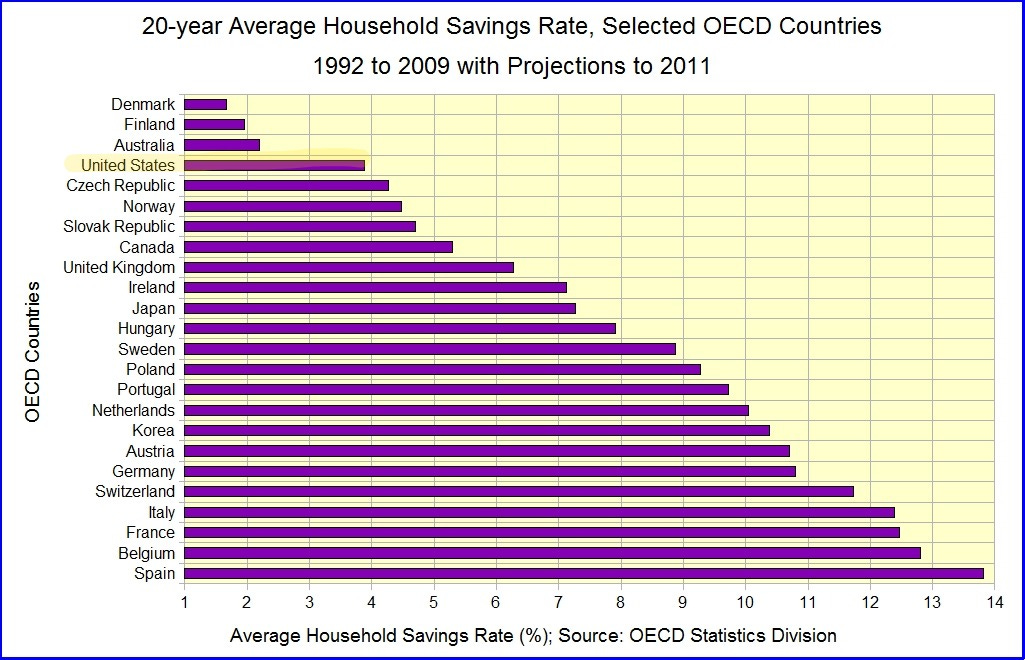

And yet, I can’t help but look at our savings rate in America in comparison to European countries, and ask myself ‘could we do better’? Household savings rates in euro area countries are higher than in America because there’s a cultural preference for financial security. Maybe we should be more like our European neighbors?

Necessity is the mother of invention, and I hope that with time, we learn to wean off the social benefits that could otherwise hold us back as a nation.

V. Conclusion

To paraphrase Lessons Of History by Will and Ariel Durant, civilizations are in a constant state of flux. What causes continued growth is the agency of creative individuals with clarity of mind and energy of will — capable of responding to new situations with good ideas to progress civilization forward.

This essay is an attempt to move the needle in a tiny way for this great nation.

(Just don’t cut social security until after my dad retires.)

Thanks for reading!

— Grant Varner

Some Interesting Ideas

Paul Krugman argues that the US doesn’t have to pay back our budget deficit. link

Noah Smith on why education, health care, and child care cost so much in America. link

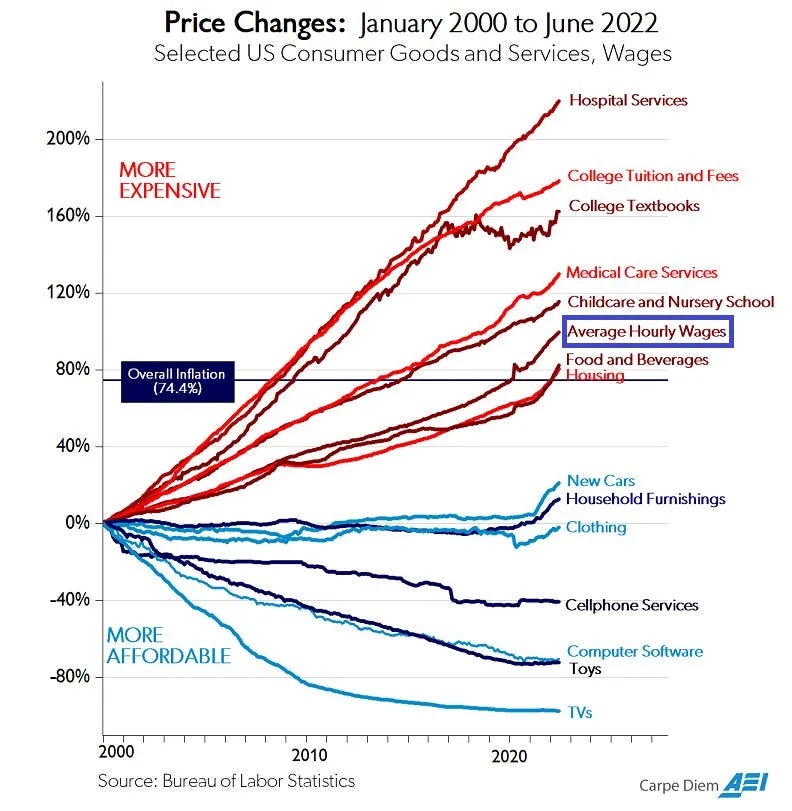

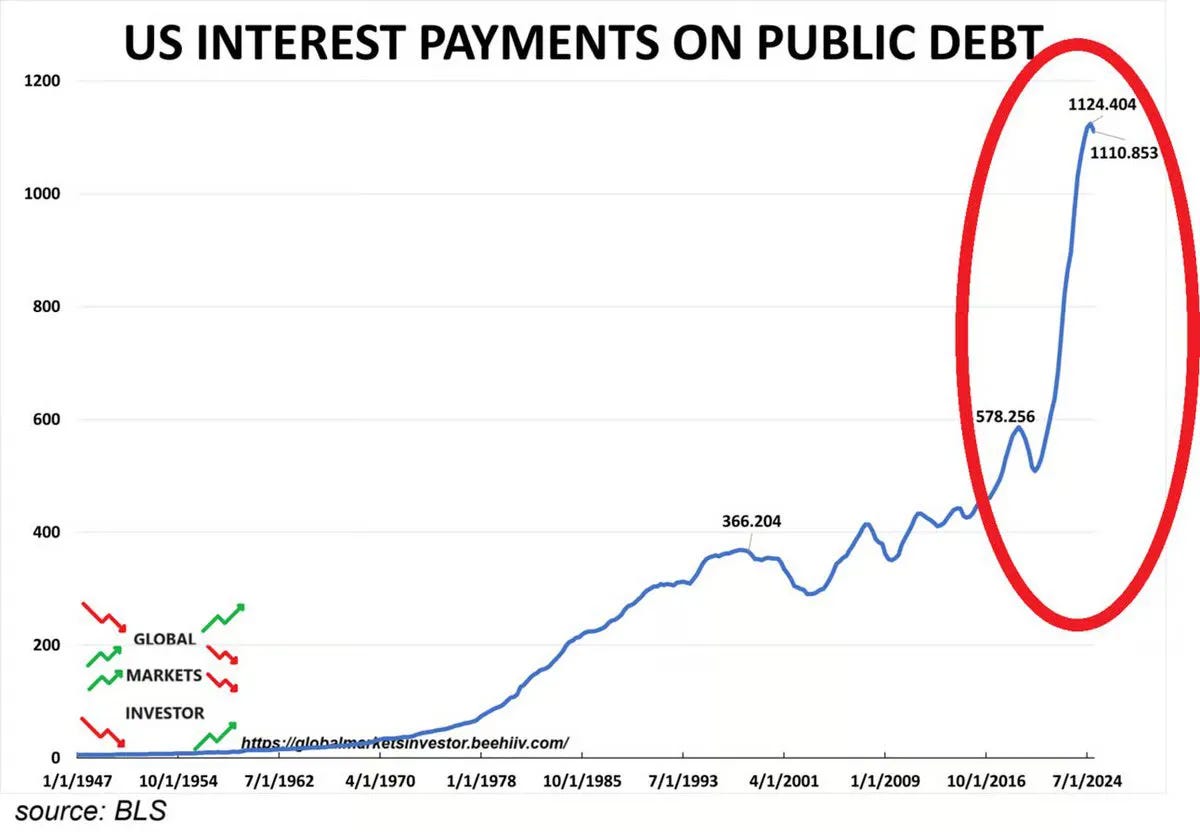

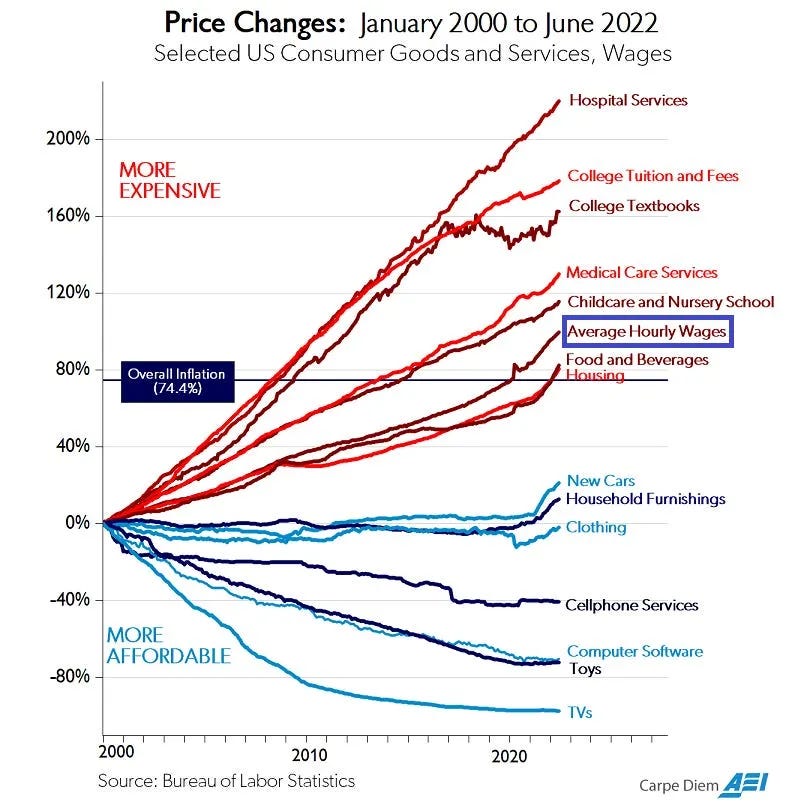

Some Interesting Charts

If social benefits were rolled back, what would be the recourse for those who have paid in but may not see the benefits?

Feels like a really difficult challenge to deal with because once folks start collecting these benefits, they aren’t going to want to see them go away.

"Which means that it’s fully backed by full trust in our country — and more accurately, the strength of our military."

This is one thing that's not fully explained here in the article - how does our military exactly support our currency? The relationship certainly doesn't seem direct