Buy Inner Peace Instead Of Passive Income

The 2008 financial crisis, the optionality of cash, and why boring investments are often the best investments.

The 2008 Financial Crisis

My parents sat my sisters and I down at the dinner table and said, “We’re moving.”

It was 2008 - the peak of the financial crisis. While I was busy trying to beat Guitar Hero 3, my parents were trying to figure out how to weather the financial storm.

I didn’t realize it at the time, but that experience shaped how I view money and risk.

Now, as an adult with my own family, I put high value on cash because of the freedom and autonomy it provides.

Cash is the antacid of personal finance. What you lose in rate of return, you gain in peace of mind.

I. Cash Is An Option To Buy Something In The Future

No one could’ve possibly predicted the COVID-19 recession. It was a black swan.

If you had invested $10,000 an index fund tracking the S&P 500 at the bottom of the COVID crash (March 23, 2020) it’d be worth about $25,000 today (March 25, 2026).

Unpredictable events create decades long buying opportunities. Cash on hand is your ticket to participate.

II. Cash Won’t Financially Ruin You

There’s a tipping point you feel when you accumulate cash savings. You feel a shift from insecurity, to security, then to abundance.

During the abundance phase, you’ll have doubts about holding cash. When in doubt, remember that:

Cash in savings accounts is FDIC-insured up to $250,000.

Everything gets cheaper during a recession.

Cash is harder to come by during a downturn.

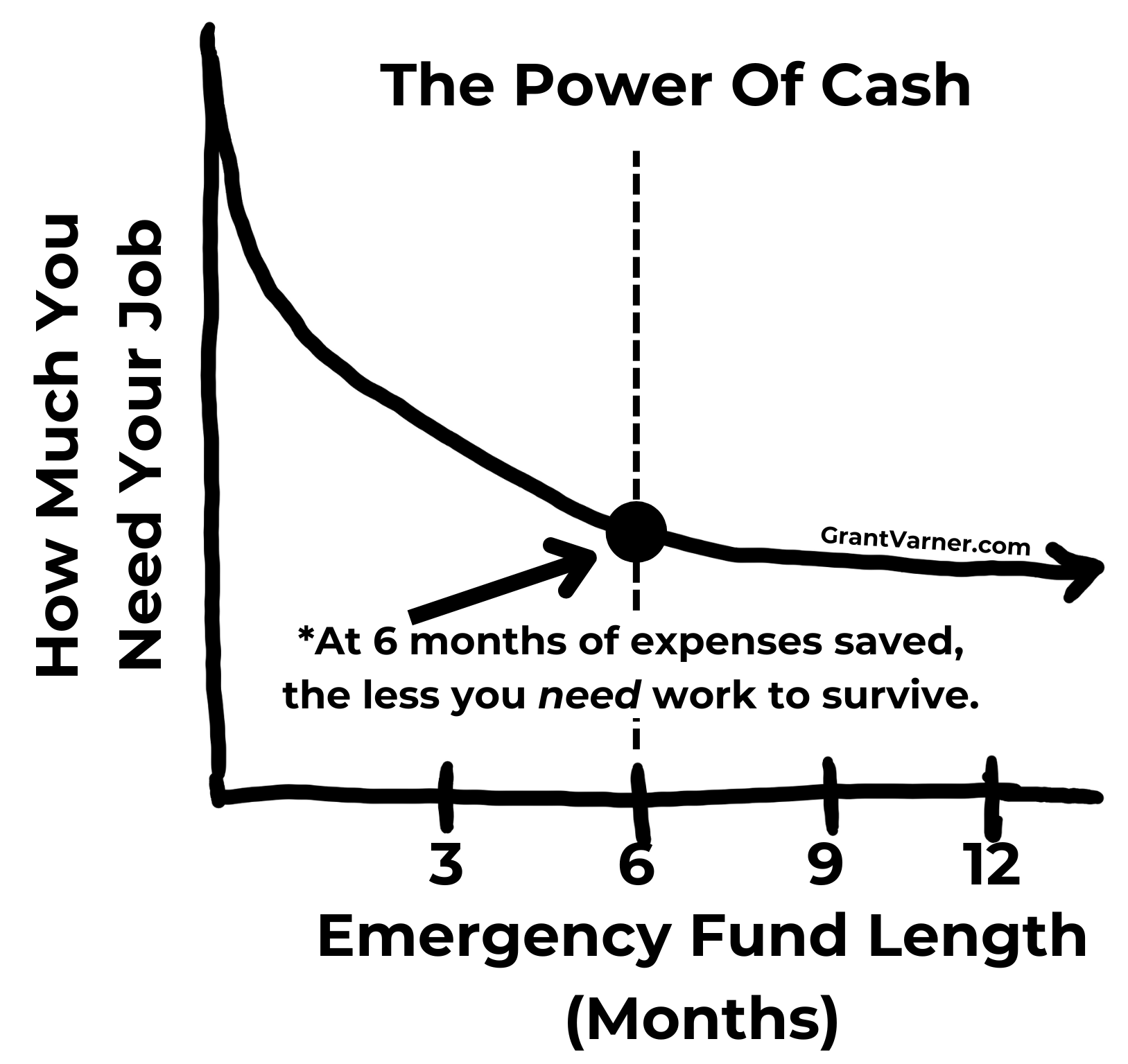

The average unemployment duration in the ‘08 recession was 6 months.

How much cash to keep comes down to your personal relationship with risk.

III. More Cash = Less Need For Work

The more cash you have saved up, the less you need to work.

When I got laid off from Oracle, I was lucky enough to get decent severance. But I’d also been saving for a while, so I had a cash cushion. My wife and I were engaged at the time, and since it was summer and she was off from school, we said, “Screw it, let’s go to Egypt.”

We flew to Egypt, stayed at a resort, spent time with her family, and lived it up. One of the best unplanned decisions we’ve made. None of it would’ve been possible without a savings buffer.

Cash gives you the opportunity to turn lemons into lemonade.

Controlling Your Time Is The Highest Dividend Money Pays

A few weeks ago, I was at my friend’s wedding. After my hundredth Swedish meatball, I started chatting with one of the groom’s friends, who owned several duplexes in Cleveland.

I asked him, “What advice would you give someone just starting out?”

He said, “Don’t get into real estate.”

He explained how he had to leave work to fix broken drains and sinks. He could’ve hired a property manager, but to make the properties cash-flow, he had to give up his time.

It got me thinking - are all dollars created equal?

Short answer: No.

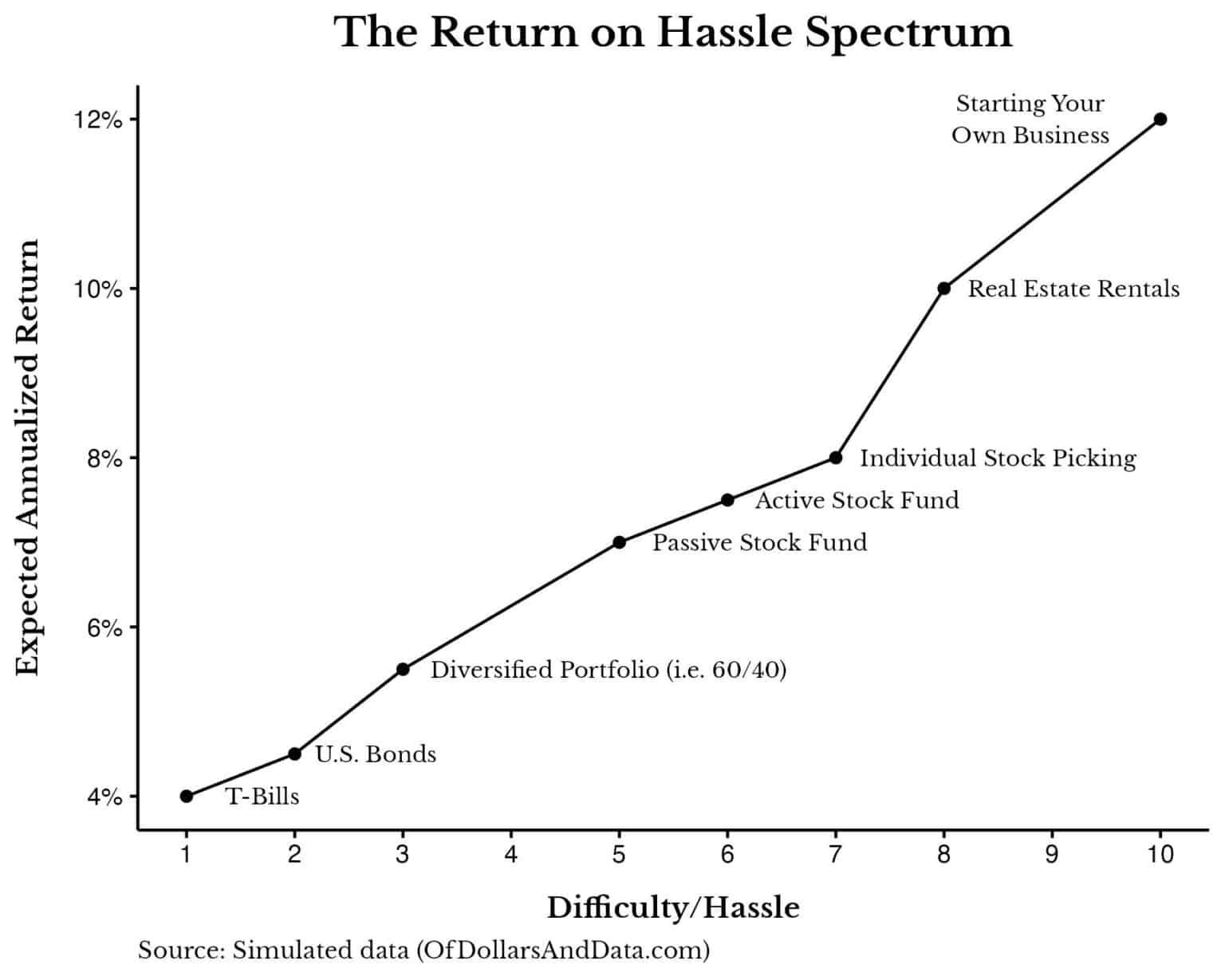

Nick Maggiulli, on his blog Of Dollars And Data, talks about the return-on-hassle spectrum. In short, not every invested dollar is created equal.

Real estate investing sounds great until you’re getting a call from a cracked-out tenant at 10 p.m. because they locked their roommate out. (True story.)

Your brokerage account will never ask any for any more of your time than it takes to click ‘sell’.

Meanwhile, my stock portfolio has never smoked crack. Or asked me to make a key copy during poker.1

(VIII) A High Earning W-2 Job Is A Cheat Code To Wealth And Freedom

When you land a high-paying, flexible W-2 job, live below your means, and invest the rest, your financial margin grows.

Over time, freedom comes builds:

Non-Mortgage Debt Paid Off: Breath a sigh of relief.

Emergency Fund: Big or small, depending on your risk profile.

Home Paid Off: You own it. No one can take it from you. Plus say goodbye to monthly house payments.

Investments Working for You: One day, your portfolio earns passively what you were earning actively (or more).

When that happens, you begin to ask: “Do I actually like my job?” And you can afford to say: “Yes, but only on these terms.”

(IX) Conclusion

If your takeaway from this post is “real estate = bad,” I didn’t do my job.

My buddy? He got his commercial real estate license. He has a passion for the space. His brother - the handyman of the duo - fixes everything. So for them, real estate is the right path.

But it’s not for me.

The main point: Real estate is not the only path to wealth. It’s just been overhyped.

The truth:

Real estate can make you rich.

Starting a business can make you rich.

A high-paying job + low cost index can make you rich.

There’s more than one way to skin a cat. Find the one that works for you.

“Happiness is the meaning and the purpose of life, the whole aim and end of human existence.” — Aristotle

The Middle Way

The purpose of money, rightly ordered, is happiness - which ironically, doesn’t involve money at all.

Risk averse cheapskate, and you’ll hoard cash without spending it.

Be a high roller who’s always keeping up with the Joneses, you risk having nothing.

One caveat here: real estate often comes with leverage and tax advantages.

Someone buying a duplex might house hack, by living in one half and use an FHA loan to put less money down. They’re investing with less upfront cash and subsidizing their own living costs.

Not every dollar invested is created equal.